Most people think loans are taken because of big problems.

A medical emergency. Job loss. A major expense.

But in reality, that’s not always how it starts.

Sometimes, the need for a loan builds quietly—through small, harmless-looking expenses that don’t feel important in the moment. And this is exactly why understanding whether you should take a loan in urgent situations is very important.

I realized this the hard way.

Not through a big financial mistake.

But through a series of tiny ones.

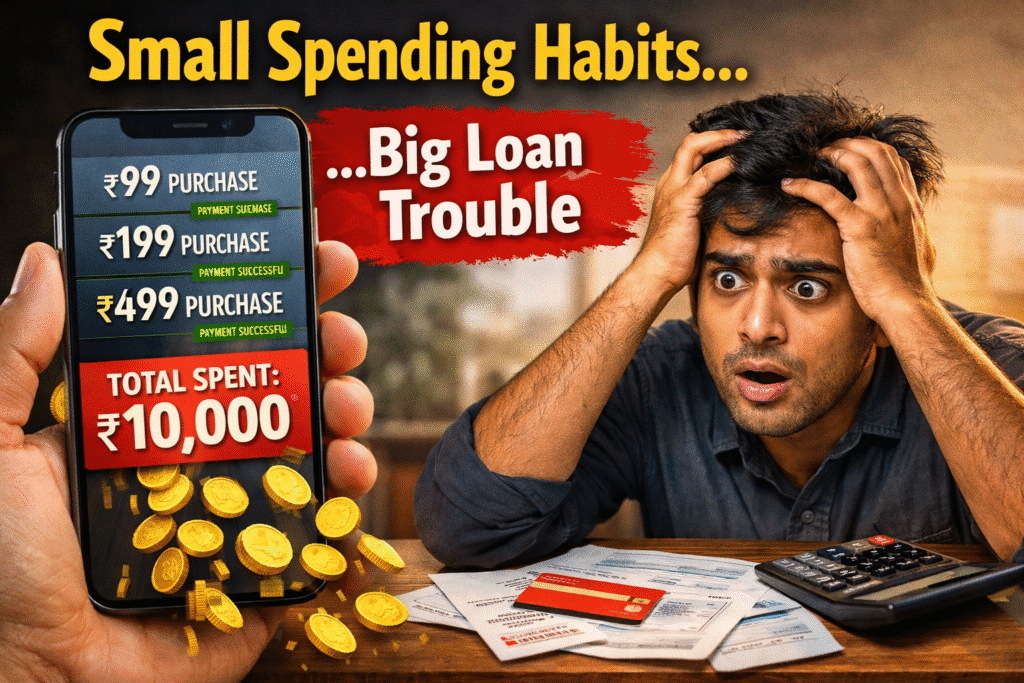

It Started With ₹99… And Didn’t Feel Like a Problem

It started with just ₹99.

A small in-app purchase while playing a mobile game. It felt harmless—like ordering a coffee or grabbing a snack.

No planning. No second thought.

Then came:

- ₹199

- ₹399

- ₹999

Each time, it felt like a small decision.

Nothing serious.

Nothing worth worrying about.

Until one day, I checked my account.

And realized I had spent ₹10,000—not on something useful, not on something necessary—but on small, repeated decisions that never felt significant individually.

Why Small Spending Feels Safe (But Isn’t)

The biggest problem with small expenses is this:

👉 They don’t trigger caution.

You don’t think:

- “Should I really do this?”

- “Can I afford this?”

Because ₹99 feels insignificant.

But over time:

Small decisions, repeated often, quietly become big financial leaks.

And the worst part?

You don’t even notice it happening.

The “Just One More” Trap

Every time I ran out of what I needed in the game, I told myself:

“Just one more… I’m almost there.”

Almost completing something

Almost winning

Almost finishing a level

That “almost” feeling creates urgency.

And urgency leads to quick decisions.

👉 Not logical ones.

How This Slowly Turns Into Financial Pressure

At first, it’s just spending.

Then slowly, something changes:

- Your savings reduce

- Your monthly buffer gets tighter

- Unexpected expenses feel heavier

And then one day, a real need comes up:

- A bill

- A repair

- A medical expense

And suddenly, you feel:

👉 “I don’t have enough right now.”

That’s when people start looking at loan apps.

This Is Where Loans Enter the Picture

Most people don’t connect this.

But it’s important:

👉 Loans are often not taken because of one big problem

👉 They are taken because of lack of available money at the wrong time

And that lack often comes from:

- Repeated small spending

- Poor tracking

- Emotional decisions

This is very similar to real-life financial mistakes people make with loan apps

A Realization That Changed My Thinking

When I saw the total amount I had spent, it wasn’t just about the money.

It was the realization that:

👉 I didn’t feel the impact while spending

👉 But I felt it all at once when I saw the total

That disconnect is dangerous.

Because it makes you believe everything is under control—until it isn’t.

Why This Matters Before Taking a Loan

Before taking a loan, most people ask:

- “Do I need this money?”

But a better question is:

👉 “Why don’t I have this money right now?”

Sometimes, the answer is a real emergency.

But sometimes, it’s:

- Untracked expenses

- Small spending habits

- Emotional decisions over time

Understanding this difference can completely change how you approach borrowing.

This Doesn’t Mean Loans Are Bad

Let’s be clear.

Loans are not the problem.

They can actually be helpful in:

- Medical emergencies

- Urgent needs

- Short-term financial gaps

But to use them correctly, you must understand how instant loans actually work and when they make sense

👉 The real issue is when loans are used to fix habits—not situations.

What You Can Do Differently

Here are a few simple but powerful changes:

✔ Start tracking small expenses

Even ₹99 matters when repeated.

✔ Set a mental spending boundary

Not every “small” purchase is harmless.

✔ Pause during urgency

If something feels like “just one more,” that’s the moment to stop.

✔ Build a small buffer

Even a basic emergency fund reduces dependency on loans.

✔ Separate needs from impulses

Not everything urgent is important.

A Simple Thought Before You Borrow

Before applying for any loan, pause and ask:

👉 “Is this a real need—or the result of small habits catching up?”

If it’s a real need → a loan can help.

If it’s a pattern → a loan may only delay the problem.

Final Thought

I didn’t spend ₹10,000 in one go.

I spent it in small amounts that didn’t feel important at the time.

That’s how most financial pressure builds—not suddenly, but silently.

Loans can be helpful tools.

But using them wisely starts with understanding why you need them in the first place.

Sometimes, the smartest financial decision isn’t taking a loan…

👉 It’s understanding what led you there.