KreditBee vs Fibe: Honest Comparison 2026 (Real User)

James D · Mumbai-based borrower

James D · Mumbai-based borrower

Real borrower — not a review site

James D has personally taken 7 loans across KreditBee and Fibe since early 2024, with real proof screenshots embedded in this article. He is currently repaying active loans on both apps. Not a financial advisor.

⚡ Quick Answer — KreditBee vs Fibe in 2026

Earn under ₹20,000/month or need cash in under 15 minutes? Go with KreditBee.

Earn ₹25,000+ and want a polished app with bigger limits? Fibe is the better fit.

Both are RBI-registered. Both disburse fast. The difference is salary eligibility and what you're borrowing for.

KreditBee vs Fibe is one of the most common questions I get — and I'm in a rare position to answer it honestly. I've personally borrowed on both since early 2024, currently repaying active loans on both, and have taken a combined seven loans across the two apps. This comparison is built entirely on that real borrowing history — not theory, not press releases.

What Are KreditBee and Fibe?

KreditBee is an instant personal loan app partnered with Krazybee Services (RBI-registered NBFC), offering loans from ₹6,000 to ₹10 lakh. Built for quick, small-ticket borrowing — accepts applicants with lower monthly incomes.

Fibe (rebranded from EarlySalary Services Private Limited) is a salary-advance and personal loan app backed by Axis Bank and Mirae Asset, rated 4.3★ on Google Play. It targets salaried professionals with structured monthly income. Both operate under RBI's digital lending framework.

My Personal Experience With KreditBee

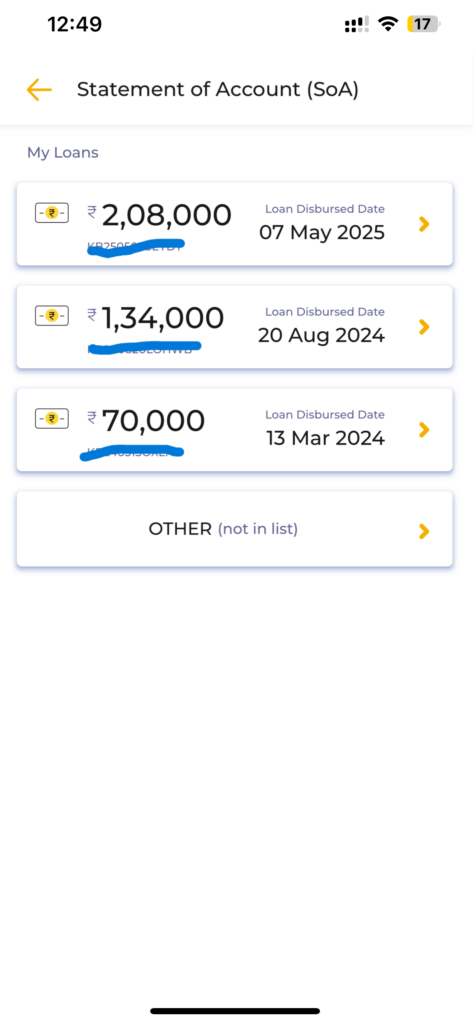

I've taken three loans on KreditBee since March 2024 — ₹70,000, then ₹1,34,000, and most recently ₹2,08,000 disbursed in May 2025. The app asked for my Aadhaar, PAN, and a selfie — no salary slip required at those loan amounts. Approval came in under 15 minutes each time and money hit my account the same day.

The interest rate on my most recent loan was around 24% p.a. — though others get closer to 20%, so it varies by profile. What I appreciate: KreditBee kept approving me as my repayment history built up, and my credit limit grew from ₹70,000 to ₹2,72,000 over two years.

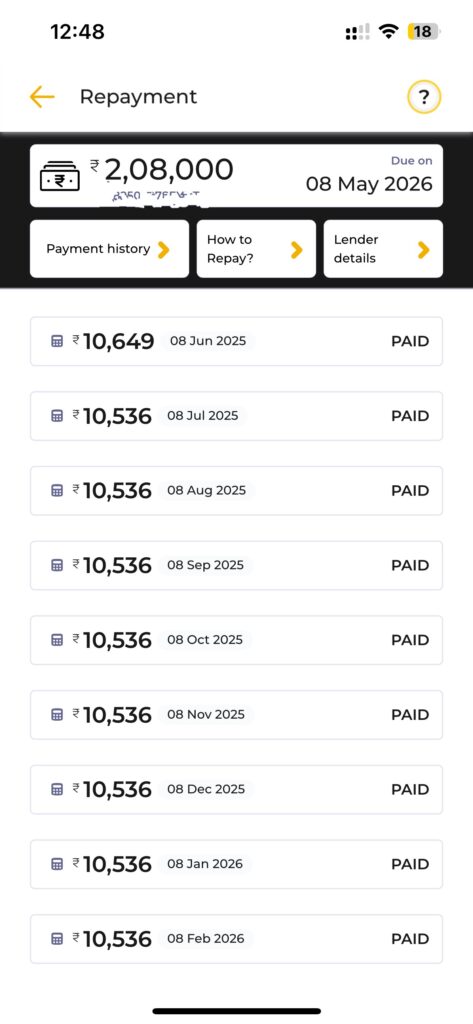

I'm currently repaying ₹10,536 per month on my active loan. As my repayment screen shows below — 9 consecutive EMIs paid, zero misses.

My Personal Experience With Fibe

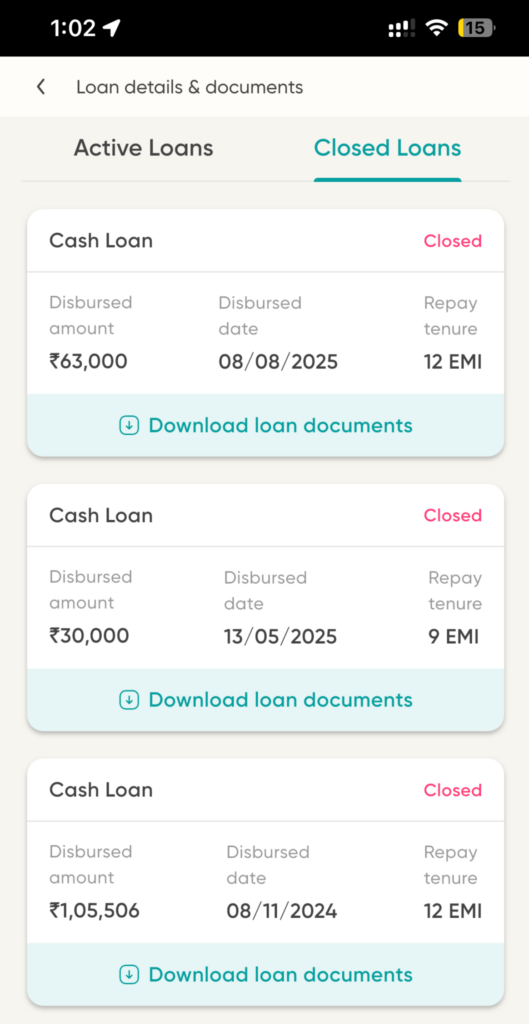

I've been using Fibe (formerly EarlySalary) since November 2024. In that time I've completed three loans — ₹1,05,506, ₹30,000, and ₹63,000 — all fully closed. I'm currently on my fourth loan of ₹62,238, with 2 of 12 EMIs paid so far.

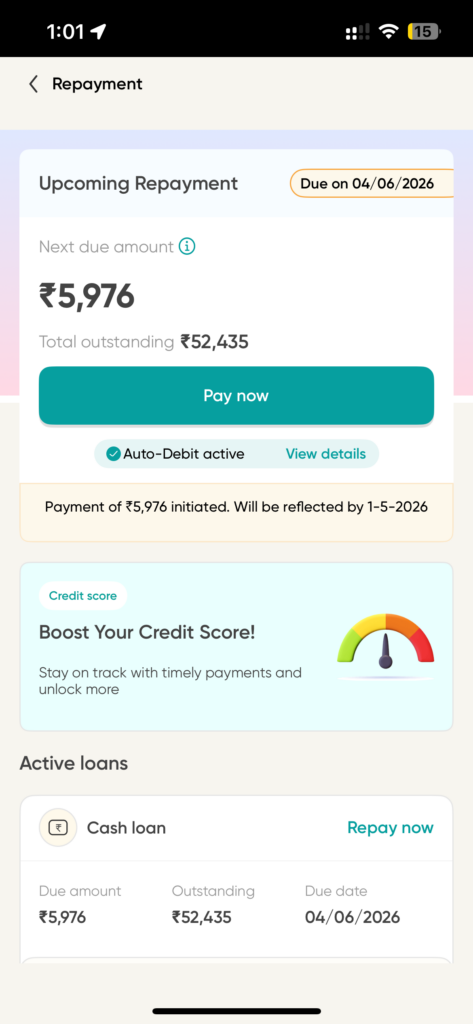

The Fibe experience is noticeably more polished than KreditBee. The interface is cleaner, onboarding is smoother, and disbursal on my most recent loan was under 2 minutes after approval. I've also set up auto-debit on Fibe — the EMI goes out automatically without me having to remember.

My current active loan has an outstanding balance of ₹52,435 with an EMI of ₹5,976 due 04 June 2026.

Always check the rate shown specifically to your profile — don't assume the advertised rate applies to you. My Fibe rate works out to ~22% p.a., but I've seen it higher for newer borrowers.

KreditBee vs Fibe: Key Comparison Table 2026

| Feature | KreditBee | Fibe |

|---|---|---|

| Loan Amount | ₹6,000 – ₹10 lakh | ₹20,000 – ₹5 lakh |

| Interest Rate | 12% – 28.5% p.a. | ~18% – 30% p.a. |

| Disbursal Speed | 10–15 minutes | Under 2 minutes |

| Min. Salary Required | ₹10,000–₹15,000/month | ₹25,000+/month |

| Play Store Rating | ~3.5★ | ~4.3★ |

| NBFC / Bank Partner | Krazybee (RBI-registered) | EarlySalary / Axis Bank |

| Processing Fee | Up to 5% | Varies by loan type |

| Salary Slip Required? | No (smaller amounts) | Yes |

| Auto-Debit Setup | Available | Excellent — very smooth |

| Best For | Quick emergency loans | EMI purchases, salary advances |

What I Liked About Each App

- Money in account in under 15 minutes — consistently

- Accepts lower salaries, accessible early-career

- Credit limit grew automatically as I repaid

- No salary slip needed for smaller amounts

- 3 loans approved, all disbursed same day

- Cleanest loan app UI I've used

- Disbursal under 2 minutes once verified

- Auto-debit setup is smooth and reliable

- Backed by Axis Bank — adds credibility

- 4.3★ Play Store rating reflects real users

Red Flags to Know Before You Apply

⚠️ KreditBee — Watch Out For

- Processing fees up to 5% make small loans expensive — always calculate the effective cost

- 3.5★ Play Store rating suggests frustrating support experiences for many users

- Short-term rates up to 28.5% p.a. are steep if you can't repay quickly

⚠️ Fibe — Watch Out For

- ₹25,000+ salary requirement shuts out a large segment of Indian borrowers

- Rates can reach 30% p.a. for lower credit profiles — always verify your specific rate

- Minimum loan amount of ₹20,000 makes it unsuitable for very small urgent needs

Who Should Use KreditBee vs Fibe

| If you… | Go with… |

|---|---|

| Earn ₹10,000–₹20,000/month | ✅ KreditBee |

| Need cash in under 15 minutes | ✅ KreditBee |

| Are a freelancer or gig worker | ✅ KreditBee |

| Have no salary slip handy | ✅ KreditBee |

| Earn ₹25,000+/month | ✅ Fibe |

| Want EMI-based purchases | ✅ Fibe |

| Want auto-debit and cleaner UI | ✅ Fibe |

| Need a loan above ₹3 lakh | ✅ KreditBee |

Final Verdict — My Personal Rating

Frequently Asked Questions