Is It Safe to Take a Loan From an App in India? 7 Questions Answered (2026)

James D

James D

Last Updated: May 2026 | By James D — Mumbai-based borrower, not a financial advisor

In 2022, I needed ₹7,000 urgently to cover a medical bill. I had a loan app open on my phone and my finger was hovering over the Apply button. Seven questions were running through my head simultaneously — will they leak my Aadhaar? Will they message my contacts if I'm late? Is it safe to take a loan from an app in India at all? I applied without answering any of them properly. The loan came through — but the recovery experience that followed when I missed one EMI was aggressive enough that I spent the next year researching every question I should have asked before clicking. Here are the honest answers.

Yes — if the app is backed by an RBI-registered NBFC, discloses all charges upfront, and doesn't request unnecessary permissions like contacts or call logs. No — if you can't verify the lending partner, if the app asks for money before disbursing, or if the reviews show aggressive recovery behaviour. Safety is not about the technology — it's about who is lending the money behind the app interface and whether they operate within RBI's digital lending guidelines.

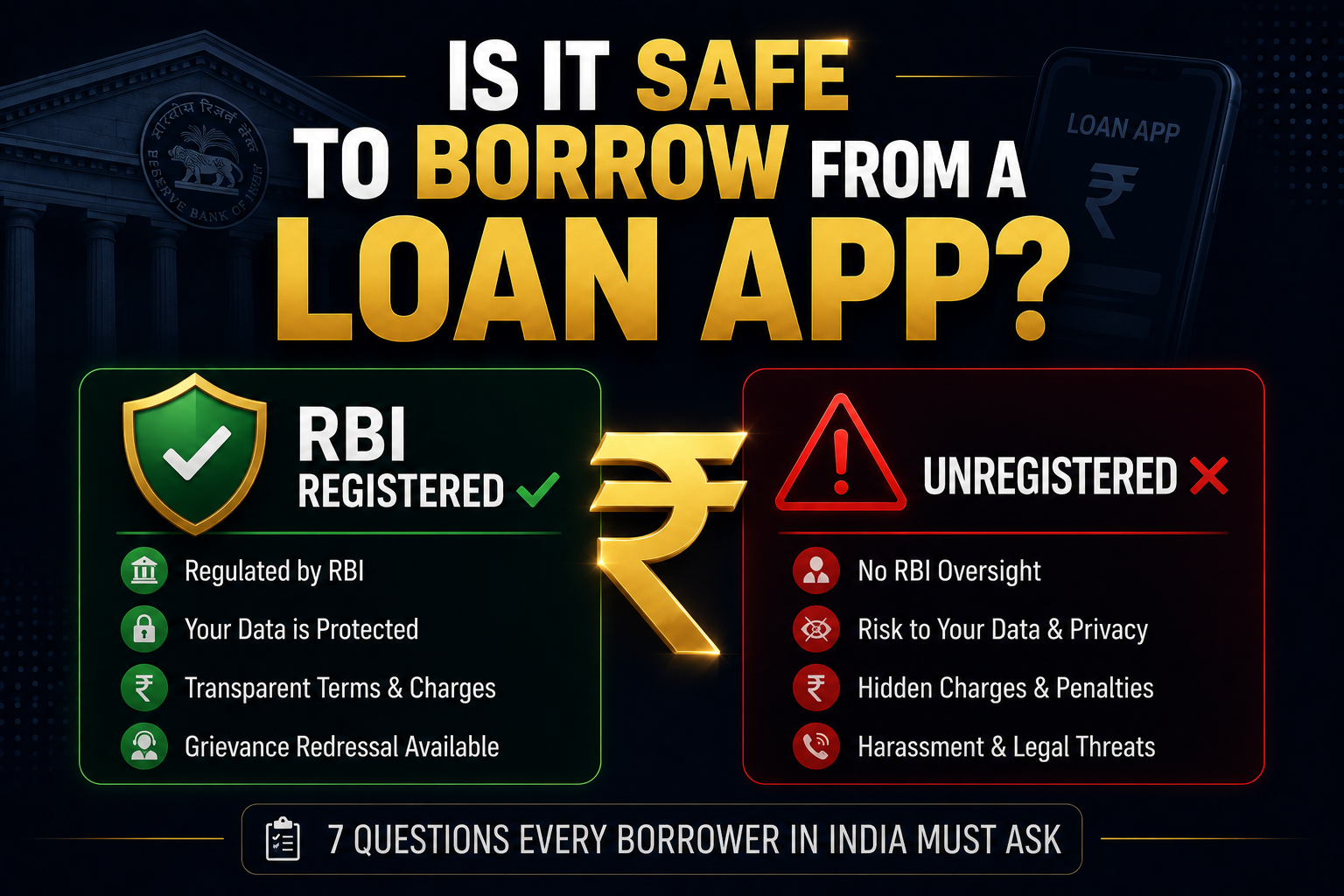

- Question 1: Is This App Actually Registered With RBI?

- Question 2: What Will They Do With My Aadhaar and PAN?

- Question 3: Why Does the App Want My Contacts and Photos?

- Question 4: What Will They Do If I Miss a Payment?

- Question 5: Will This Affect My CIBIL Score?

- Question 6: Am I Getting the Full Amount I Applied For?

- Question 7: Are There Red Flags I Should Walk Away From?

- The Pre-Apply Checklist

- GetLoanCredit Verdict

- Frequently Asked Questions

Question 1: Is This App Actually Registered With RBI?

This is the single most important question — and most borrowers never ask it. The app itself is not registered with RBI. The NBFC lending money through the app is. A safe app names its NBFC lending partner clearly in the Terms and Conditions or About section.

Once you have that name, verify it at rbi.org.in → Financial Entities → NBFC list. If the company appears there, you're dealing with a regulated lender. If the app names no lending partner — or the name doesn't appear on the RBI site — stop and find a different app.

KreditBee's partner is Krazybee Services Private Limited. Nira's is Muthoot Microfin. Both are on the RBI list. Both took me under 3 minutes to verify.

Question 2: What Will They Do With My Aadhaar and PAN?

RBI-registered NBFCs are legally required to protect your KYC data under the IT Act and RBI's digital lending guidelines. They can use it only for identity verification and credit assessment — not for marketing, sharing with third parties, or any other purpose without your explicit consent.

Unregistered apps have no such obligation. If you share your Aadhaar and PAN with an app that has no named, verifiable NBFC behind it, that data can be misused for identity fraud. The risk is not from KYC itself — it's from sharing KYC with unverified entities. Verify first, share second. Never the other way around.

Question 3: Why Does the App Want Access to My Contacts and Photos?

It shouldn't — and if it does, that's your answer. A legitimate loan app needs camera access for your KYC selfie and storage access for document upload. That is all. It does not need your contacts, call logs, gallery, microphone, or location to disburse or recover a loan.

Apps that request contact access use it for one purpose during recovery: to message your friends, family, and colleagues if you miss a payment. This is illegal under RBI's 2022 digital lending guidelines — but it happens because many borrowers grant the permission without reading what they're agreeing to.

Before installing any app, check the permissions it will request. If contacts, call logs, or gallery appear — do not install it. This one check eliminates the vast majority of predatory apps immediately.

Question 4: What Will They Do If I Miss a Payment?

For RBI-registered apps, the legal recovery process is: reminder calls during business hours (8am–7pm), SMS and app notifications, late fees as disclosed in the loan agreement, and CIBIL reporting after 30–45 days. That is it. Anything beyond that — calling outside hours, abusive language, contacting your network — is illegal and reportable.

The practical answer: look at the reviews. Sort by lowest rating and look specifically for descriptions of what happened when borrowers were late. Specific, detailed negative reviews about recovery behaviour are the most reliable signal of what you'll experience if repayment becomes difficult. Generic positive reviews tell you very little.

Question 5: Will This Affect My CIBIL Score?

Yes — in two ways. First, the application creates a hard inquiry that drops your score by 5–10 points temporarily. Second, the repayment outcome — positive or negative — is reported to CIBIL if the app is backed by an RBI-registered NBFC.

This cuts both ways. Repay on time and your score improves — I gained 12 points from my first clean repayment on Nira. Miss a payment and your score drops by 30–70 points depending on your starting score and the length of the default. The CIBIL impact is real, meaningful, and lasts months. Factor it into your decision before applying.

Question 6: Am I Actually Getting the Full Amount I Applied For?

Almost certainly not. Processing fees of 1–5% plus 18% GST are deducted before disbursal on most apps. On a ₹10,000 loan, you typically receive ₹9,400–₹9,700. You repay the full ₹10,000 plus interest regardless.

Before accepting any loan offer, look for the disbursement amount — not the loan amount. RBI guidelines require this to be shown clearly in the Key Fact Statement before you accept. If the app doesn't show you the exact amount that will hit your account before you tap Accept, don't proceed.

On a ₹10,000 loan with a 3% processing fee + GST, you receive approximately ₹9,469 — but you repay the full ₹10,000 plus interest. Always check the disbursement amount before accepting.

Question 7: Are There Red Flags I Should Walk Away From?

| Red Flag | What It Means | Action |

|---|---|---|

| No named NBFC lending partner | Unregistered or illegal operation | Do not apply |

| Requests contacts or call log access | Will use for harassment during recovery | Do not install |

| Asks for fee before disbursing loan | Fee collection scam — no real loan | Report to cybercrime.gov.in |

| "Guaranteed approval" claims | No legitimate lender can guarantee this | Treat as red flag |

| No working customer support | No accountability if things go wrong | Do not apply |

| Reviews show aggressive recovery | Legal recovery process is being violated | Choose a different app |

If any two of these apply — walk away. There are enough legitimate, verifiable apps that you never need to compromise on any one of these, let alone two.

The Pre-Apply Checklist — Answer These Before Every Application

- NBFC lending partner named and verified on rbi.org.in

- Permissions are camera and storage only

- All charges shown upfront before acceptance

- Disbursement amount (not loan amount) confirmed

- Reviews include specific, genuine borrower experiences

- Repayment source confirmed — salary date, client payment, known income

⭐ GetLoanCredit Verdict

| Factor | Assessment |

|---|---|

| Safety of RBI-registered loan apps | ⭐⭐⭐⭐☆ — strong with verification |

| Risk from unregistered apps | ⚠️ Very high — avoid entirely |

| Data safety with verified apps | ⭐⭐⭐⭐☆ — legally protected |

| CIBIL impact if repaid on time | ⭐⭐⭐⭐⭐ — meaningful positive |

| Worth 15 minutes of verification | ⭐⭐⭐⭐⭐ — always, no exceptions |

It is safe to take a loan from an app in India — but only from the right app, applied to in the right situation, with a confirmed repayment plan. The 7 questions above take 15 minutes to answer. That 15 minutes has more impact on your financial safety than anything else you can do before clicking Apply.

Don't skip it because you're in a hurry. The urgency is exactly what predatory apps rely on.

Frequently Asked Questions